China's Intelligent Warfare and Dual Industrial Structure

.

Member of Policy Proposal Committee of JFSS Koji Hirai

China's Industrial Structure

To understand the reason why Japan has to maintain a certain extent of separation from China, we need to know about its policy and structure of industry. TEIKOKU DATABANK, LTD., a Japanese research company of markets and corporations, reported that 13,646 Japanese companies have joined the Chinese markets as of January 2020, few of which companies have learned the industrial policy and structure peculiar to China.

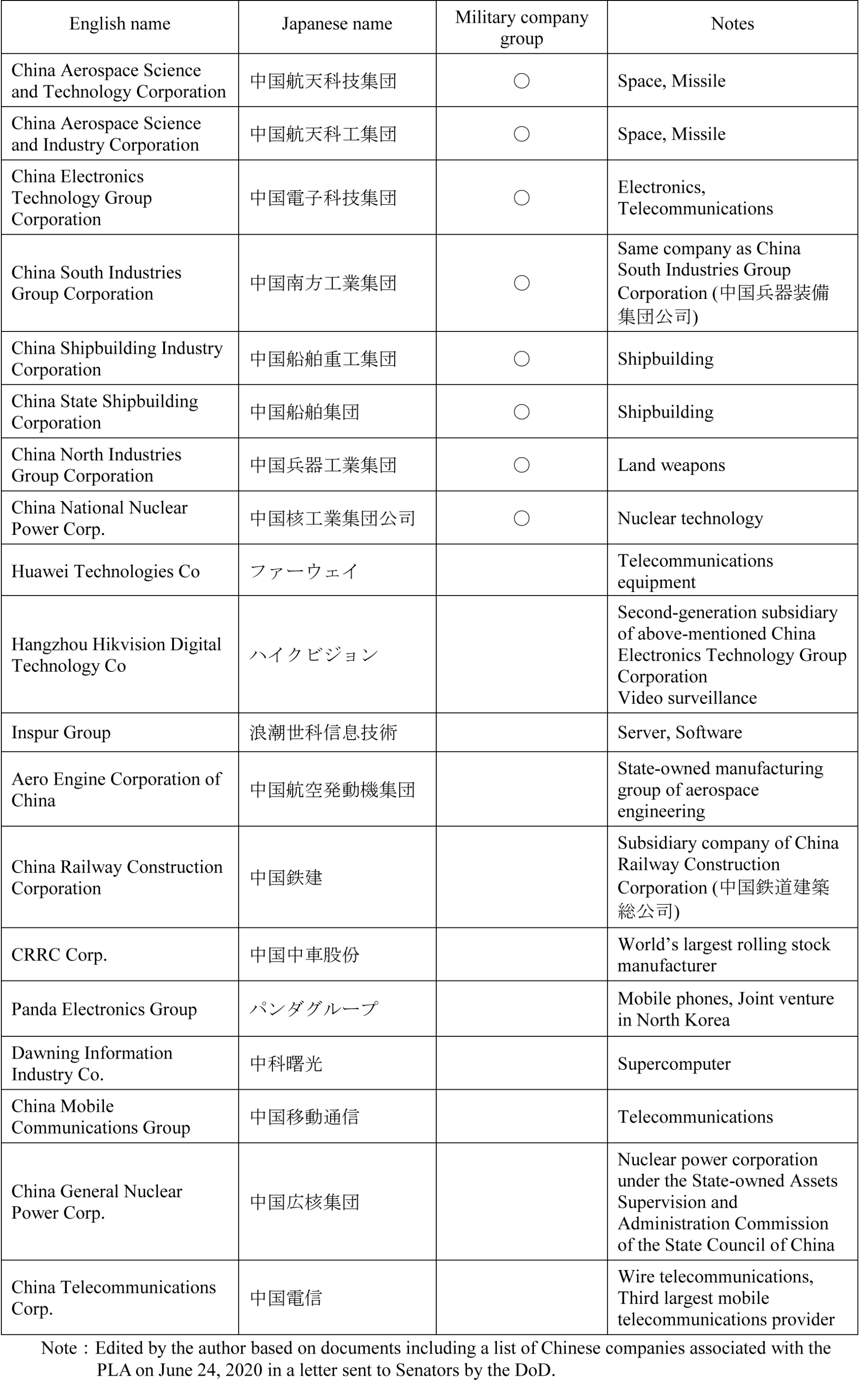

China is a country that integrates its military expansion and economic growth. A character of Chinese industrial structure is that the People's Liberation Army (PLA), the Chinese government and some military company groups have formed an alliance in the field of politics, economy and military. On June 24 of 2020, the United States Department of Defense (DoD) made, in a letter sent to Senators, a list of twenty Chinese companies including Huawei that are associated with the PLA. The table below shows the military company groups.

Table:Chinese military companies in U.S.

These military company groups have played a central role in research development and manufacturing of the PLA's weapons and equipment. Some companies under the military companies have converted military technologies into commercial sector and, since 2005, others have applied civil technologies to military ones after civil companies were permitted to enter the military field.

If a Chinese military company is a parent one whose subsidiary company seems to manufacture only civil products, dual-use technologies can be completely leaked out through the subsidiary company. As a result, Japanese companies can face the risk of being utilized for China’s civil-military integration strategy without noticing.

“The civil-military integration,” an industrial policy of China, means that the military technologies are developed in aiming to be applied to civil products. Under the policy, China can achieve its large economic growth through commercialization and sale of the products that the military technologies are translated into.

While Japanese media has not told the most important issue, Japanese companies are also operating their business in China, neglecting the civil-military integration.

In Japan, the transfer of dual-use technologies and products is restricted by the Export Trade Control Order and the Foreign Exchange Order, both of which are based on the Foreign Exchange and Foreign Trade Act (FEFTA). Therefore, Japanese companies, universities and research institutions are required to have strict management of their technologies not to be converted into China's military products. Besides, after the Foreign Exchange and Foreign Trade Act were substantially modified last year, Japan has restricted the overseas transfer more rigid, and the act has become as severe as the U.S. Foreign Investment Risk Review Modernization Act of 2018 (FIRRMA), which is contained in the National Defense Authorization Act for Fiscal Year 2019.

Although Japanese companies, especially in restricted industry, have to pay careful attention, the small and medium enterprises are, at present, not informed of the details of revisions. Under this circumstance, if they have a deal with Chinese private companies regarding the dual-use technologies, there are two obvious risks as below;

1. a risk that China converts into weapons the technologies and products imported from Japanese companies which have a deal, establish a joint venture or have a technology partnership with Chinese companies.

2. a risk that China resells its dual-use products or transfers its dual-use technologies to third countries with security concerns.

We can't use any excuse, for example, “We didn't know about the FEFTA.” It is vital that Japanese small and medium enterprises hold counsel with the specialized institutions or outside experts if they operate business in China with little knowledge of export management.

Reasons for transfer of dual-use technologies

We have been witnessing outstanding development of the information and communication technology, a collective term for information processing and communications technology used for PCs and smartphones. Also, in the military field, the information and communications system plays a central role in connecting equipment to command system. Being aware of this, China came to uphold “the Intelligent Warfare” from around 2017. In China's defense white paper, we can read its purposes of use of dual-use technologies transferred from the Western developing countries.

“Driven by the new round of technological and industrial revolution, the application of cutting-edge technologies such as artificial intelligence (AI), quantum information, big data, cloud computing and the Internet of Things is gathering pace in the military field. International military competition is undergoing historic changes.”

“To safeguard China's maritime rights and interests; to safeguard China's security interests in outer space, electromagnetic space and cyberspace; to safeguard China's overseas interests; and to support the sustainable development of the country.”

Moreover, regarding the artificial intelligence development plan, China argues that it promotes the conversion of artificial intelligence technology into dual-use, strengths a new generation of artificial intelligence technology into a powerful pillar for command, military simulations, defense equipment, and guides both conversion and application of achievements of artificial intelligence in defense domain into civilian use.

To grasp the hegemonic power from the U.S., China has regarded “control of intelligence” as an essential factor in addition to control of the sea and the air in warfare. And to strengthen its control of intelligence, China has, by all possible means, acquired dual-use technologies from the West, and converted and utilized them for modernization of the weapons because a result of the intelligent warfare depends upon national overall scientific and technological capabilities. The purpose is that using intelligent weapons based on Internet of Things (IoT), China can proceed with conversion into military equipment corresponding to integrated warfare in land, sea, air, outer space, electromagnetic, cyber and intellectual domains.

While the dual-use technologies and products have been converted to weaponry such as nuclear and biological weapons, missiles, automatic rifles, tanks and fighter aircrafts, China will be going to improve and reinforce PLA's main weapons such as Type 15 tank, Type 052D destroyer, Chengdu J-20 (fifth-generation fighter aircraft) and DF-26 (intermediate-range ballistic missile) into typical intelligent weapons.

For the reasons above, the Chinese government, at National People's Congress in 2020, announced that it set its defense budget growth target at 6.6 percent increase year-on-year, resulting in 1.268 trillion yuan ($185.7 billion), arguing that it would firmly pursue military expansion in spite of economic stagnation.

Made in China 2025 and China's market

In 2015, China announced its new industrial policy named “Made in China 2025,” which discusses military and civilian infusion and preparation for intelligence warfare, unveiling its ambition to surpass the U.S. and to become the world's largest and strongest manufacturing country. The details are in its “Priority Domain Technology Roadmap” as below.

“By 2025, China will establish an industrial structure and technological innovation systems for core information equipment in the field of advanced intelligence, and acquire the capability for providing over 60% of core information equipment in the field of intelligence supplied by the domestic market.”

The key industry sectors that the Chinese government targets are ①New Information and Communications Technology (ICT) Industry including semiconductors, ②Advanced Numerical Control Machine Tools and Robotics, ③Aerospace, ④Ocean Engineering Equipment and High-tech ships, ⑤Advanced Rail Transit Equipment, ⑥Energy Saving and Smart Vehicles, ⑦Electricity Equipment, ⑧Agriculture Equipment, ⑨New Materials and ⑩Biopharmaceuticals and High-performance Medical Equipment. All of these sectors are essential for China to overcome the U.S. in intelligence warfare.

Japanese companies, however, have yet to be liberated from the sticky fantasy such as “China boasts the world's largest population” and “China has a great and fascinating demand for Japanese products.” We should remember that what happened to Japanese factories and commercial facilities in China after the Japanese government had nationalized the Senkaku Islands. In Chinese markets, the market share has little connection with factors such as quality and prices of products because, unlike the Western markets, the Chinese markets are closed and under control of the government. In case that the conflict between the U.S. and China gets more aggravated and Japan declares its support for the former, the market share of Japanese companies will be highly likely to be decreased radically by Chinese government's orders. In my view, it is unreasonable to assume that in a country with a large population but an authoritarian regime, we can engage in the same business-to-business competition as the Western markets.

China has professed, in its “Made in China 2025,” that it will have been a global manufacturing superpower by 2049, and Japanese companies would be disvalued if its goal is achieved. Many corporate managers and economic analysts ignore or understate possibility that their companies would be discarded after they and their expertise are transferred to China.

Moreover, Japanese companies are negative for relocating their production bases to Japan because they believe that the ratio of Chinese parts is unable to be lowered quickly with accessibility to various and cheaper parts of Chinese manufacturers. However, can Japan's supply chains be maintained and operated if the Chinese government orders that its parts suppliers should not provide their products to Japan?

I have described above the China's industrial structure, its reason for transfer of dual-use technologies and its industrial policy. Taking into consideration the possibility that pro-China companies would be imposed strict economic sanctions from the U.S., it is required that Japan stop disclosure of its invaluable technologies and secure its dominant competitiveness for its companies' survival. Besides, remember to prevent transfer of dual-use technologies in terms of national security and to review global supply chains for less dependence upon the Chinese markets.

Nevertheless, we have no choice but to accept the reality that many Japanese companies have difficulties to take actions to be apart from China by themselves due to their internal matters while the government urges them to do so. The Japanese government, therefore, is expected to have a leading role in accomplishing de-Sinicization. In the next 202nd session of the Diet, as well as discussing economic security, the government must encourage Japanese companies to de-Sinicize, especially in the regulated industries specified in the FEFTA. Since the U.S. presidential election is scheduled in November of 2020, the next year will be extremely important for Japanese industries.

原文はこちら

These military company groups have played a central role in research development and manufacturing of the PLA's weapons and equipment. Some companies under the military companies have converted military technologies into commercial sector and, since 2005, others have applied civil technologies to military ones after civil companies were permitted to enter the military field.

If a Chinese military company is a parent one whose subsidiary company seems to manufacture only civil products, dual-use technologies can be completely leaked out through the subsidiary company. As a result, Japanese companies can face the risk of being utilized for China’s civil-military integration strategy without noticing.

“The civil-military integration,” an industrial policy of China, means that the military technologies are developed in aiming to be applied to civil products. Under the policy, China can achieve its large economic growth through commercialization and sale of the products that the military technologies are translated into.

While Japanese media has not told the most important issue, Japanese companies are also operating their business in China, neglecting the civil-military integration.

In Japan, the transfer of dual-use technologies and products is restricted by the Export Trade Control Order and the Foreign Exchange Order, both of which are based on the Foreign Exchange and Foreign Trade Act (FEFTA). Therefore, Japanese companies, universities and research institutions are required to have strict management of their technologies not to be converted into China's military products. Besides, after the Foreign Exchange and Foreign Trade Act were substantially modified last year, Japan has restricted the overseas transfer more rigid, and the act has become as severe as the U.S. Foreign Investment Risk Review Modernization Act of 2018 (FIRRMA), which is contained in the National Defense Authorization Act for Fiscal Year 2019.

Although Japanese companies, especially in restricted industry, have to pay careful attention, the small and medium enterprises are, at present, not informed of the details of revisions. Under this circumstance, if they have a deal with Chinese private companies regarding the dual-use technologies, there are two obvious risks as below;

1. a risk that China converts into weapons the technologies and products imported from Japanese companies which have a deal, establish a joint venture or have a technology partnership with Chinese companies.

2. a risk that China resells its dual-use products or transfers its dual-use technologies to third countries with security concerns.

We can't use any excuse, for example, “We didn't know about the FEFTA.” It is vital that Japanese small and medium enterprises hold counsel with the specialized institutions or outside experts if they operate business in China with little knowledge of export management.

Reasons for transfer of dual-use technologies

We have been witnessing outstanding development of the information and communication technology, a collective term for information processing and communications technology used for PCs and smartphones. Also, in the military field, the information and communications system plays a central role in connecting equipment to command system. Being aware of this, China came to uphold “the Intelligent Warfare” from around 2017. In China's defense white paper, we can read its purposes of use of dual-use technologies transferred from the Western developing countries.

“Driven by the new round of technological and industrial revolution, the application of cutting-edge technologies such as artificial intelligence (AI), quantum information, big data, cloud computing and the Internet of Things is gathering pace in the military field. International military competition is undergoing historic changes.”

“To safeguard China's maritime rights and interests; to safeguard China's security interests in outer space, electromagnetic space and cyberspace; to safeguard China's overseas interests; and to support the sustainable development of the country.”

Moreover, regarding the artificial intelligence development plan, China argues that it promotes the conversion of artificial intelligence technology into dual-use, strengths a new generation of artificial intelligence technology into a powerful pillar for command, military simulations, defense equipment, and guides both conversion and application of achievements of artificial intelligence in defense domain into civilian use.

To grasp the hegemonic power from the U.S., China has regarded “control of intelligence” as an essential factor in addition to control of the sea and the air in warfare. And to strengthen its control of intelligence, China has, by all possible means, acquired dual-use technologies from the West, and converted and utilized them for modernization of the weapons because a result of the intelligent warfare depends upon national overall scientific and technological capabilities. The purpose is that using intelligent weapons based on Internet of Things (IoT), China can proceed with conversion into military equipment corresponding to integrated warfare in land, sea, air, outer space, electromagnetic, cyber and intellectual domains.

While the dual-use technologies and products have been converted to weaponry such as nuclear and biological weapons, missiles, automatic rifles, tanks and fighter aircrafts, China will be going to improve and reinforce PLA's main weapons such as Type 15 tank, Type 052D destroyer, Chengdu J-20 (fifth-generation fighter aircraft) and DF-26 (intermediate-range ballistic missile) into typical intelligent weapons.

For the reasons above, the Chinese government, at National People's Congress in 2020, announced that it set its defense budget growth target at 6.6 percent increase year-on-year, resulting in 1.268 trillion yuan ($185.7 billion), arguing that it would firmly pursue military expansion in spite of economic stagnation.

Made in China 2025 and China's market

In 2015, China announced its new industrial policy named “Made in China 2025,” which discusses military and civilian infusion and preparation for intelligence warfare, unveiling its ambition to surpass the U.S. and to become the world's largest and strongest manufacturing country. The details are in its “Priority Domain Technology Roadmap” as below.

“By 2025, China will establish an industrial structure and technological innovation systems for core information equipment in the field of advanced intelligence, and acquire the capability for providing over 60% of core information equipment in the field of intelligence supplied by the domestic market.”

The key industry sectors that the Chinese government targets are ①New Information and Communications Technology (ICT) Industry including semiconductors, ②Advanced Numerical Control Machine Tools and Robotics, ③Aerospace, ④Ocean Engineering Equipment and High-tech ships, ⑤Advanced Rail Transit Equipment, ⑥Energy Saving and Smart Vehicles, ⑦Electricity Equipment, ⑧Agriculture Equipment, ⑨New Materials and ⑩Biopharmaceuticals and High-performance Medical Equipment. All of these sectors are essential for China to overcome the U.S. in intelligence warfare.

Japanese companies, however, have yet to be liberated from the sticky fantasy such as “China boasts the world's largest population” and “China has a great and fascinating demand for Japanese products.” We should remember that what happened to Japanese factories and commercial facilities in China after the Japanese government had nationalized the Senkaku Islands. In Chinese markets, the market share has little connection with factors such as quality and prices of products because, unlike the Western markets, the Chinese markets are closed and under control of the government. In case that the conflict between the U.S. and China gets more aggravated and Japan declares its support for the former, the market share of Japanese companies will be highly likely to be decreased radically by Chinese government's orders. In my view, it is unreasonable to assume that in a country with a large population but an authoritarian regime, we can engage in the same business-to-business competition as the Western markets.

China has professed, in its “Made in China 2025,” that it will have been a global manufacturing superpower by 2049, and Japanese companies would be disvalued if its goal is achieved. Many corporate managers and economic analysts ignore or understate possibility that their companies would be discarded after they and their expertise are transferred to China.

Moreover, Japanese companies are negative for relocating their production bases to Japan because they believe that the ratio of Chinese parts is unable to be lowered quickly with accessibility to various and cheaper parts of Chinese manufacturers. However, can Japan's supply chains be maintained and operated if the Chinese government orders that its parts suppliers should not provide their products to Japan?

I have described above the China's industrial structure, its reason for transfer of dual-use technologies and its industrial policy. Taking into consideration the possibility that pro-China companies would be imposed strict economic sanctions from the U.S., it is required that Japan stop disclosure of its invaluable technologies and secure its dominant competitiveness for its companies' survival. Besides, remember to prevent transfer of dual-use technologies in terms of national security and to review global supply chains for less dependence upon the Chinese markets.

Nevertheless, we have no choice but to accept the reality that many Japanese companies have difficulties to take actions to be apart from China by themselves due to their internal matters while the government urges them to do so. The Japanese government, therefore, is expected to have a leading role in accomplishing de-Sinicization. In the next 202nd session of the Diet, as well as discussing economic security, the government must encourage Japanese companies to de-Sinicize, especially in the regulated industries specified in the FEFTA. Since the U.S. presidential election is scheduled in November of 2020, the next year will be extremely important for Japanese industries.

原文はこちら